Minister of Finance Margaret Mwanakatwe has painted a bright future for Zambia’s economy in the coming year. In a statement issued to the media today said on Preliminary Review of the Performance of the Zambian Economy in 2018, the Minister said that Zambia’s economy in 2018 remained generally resilient despite a number of challenges, with 2018 growth showing a positive momentum with quarterly GDP trending upwards.

The Minister said that in 2019, macroeconomic stability is projected to be sustained, aided by continued implementation of reforms and policies to support delivery of fiscal consolidation for sustainable and inclusive growth. The Minister called on all stakeholders to commit to the legal reforms and the measures outlined in the economic stabilisation and growth programme in order to sustain growth and create wealth

Below is the full statement

STATEMENT BY THE MINISTER OF FINANCE Mrs. MARGARET D. MWANAKATWE, MCC, MP, ON PRELIMINARY REVIEW OF THE PERFORMANCE OF THE ECONOMY IN 2018 AND OUTLOOK FOR 2019

OVERVIEW

Economic performance in 2018 remained generally resilient. The performance was supported by relative macroeconomic stability as well as less volatile commodity prices particularly for copper. This notwithstanding, several downside risks to the economic performance encountered included: continued global trade tension; and, rise in global oil prices. On the domestic front, negative market sentiment related to fiscal challenges; upward adjusted debt; sluggish credit growth; depreciation of the Kwacha from the third quarter which triggered inflationary pressures; and, lower than anticipated agriculture output arising from the poor rainfall, impacted on the overall performance of the economy.

DEVELOPMENTS IN THE DOMESTIC ECONOMY IN 2018

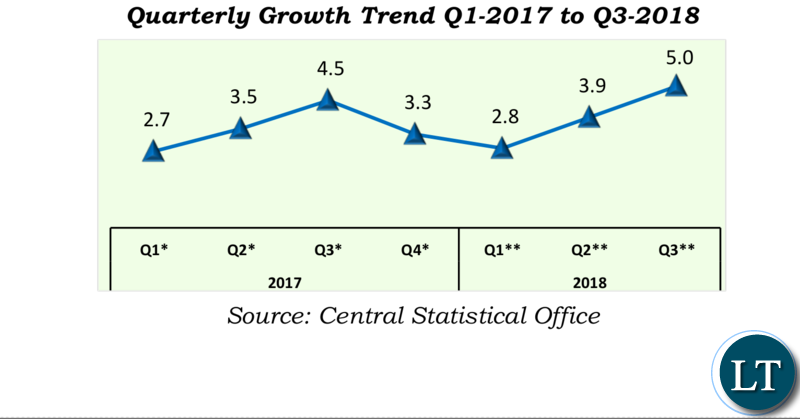

Growth momentum remained positive in 2018 – Growth in 2018 showed positive momentum with quarterly GDP trending upwards. Preliminary growth estimates indicated a pick-up in the third quarter to 5.0 % from 3.9% and 2.7 % in second and first quarters (figure 1). The buoyant performance in mining, manufacturing and construction as well as stable supply of electricity aided the growth momentum in 2018. The annual growth is expected to remain robust around 4% albeit slower than year projection on account of poor performance of the agriculture sector as well as weak credit growth to the private sector and continued elevation in non-performing loans.

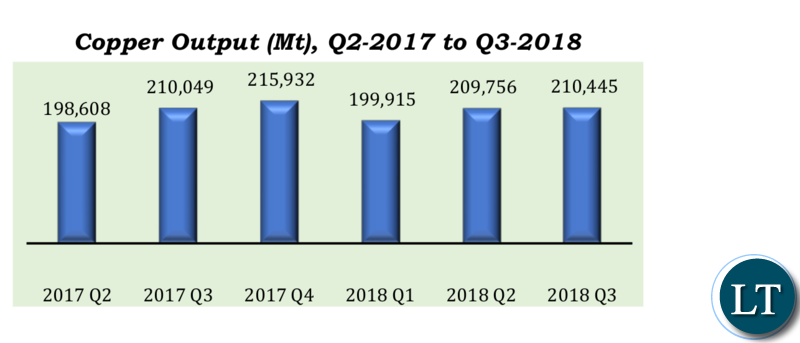

Copper output in 2018 continued to increase with a total of 696,526 Mt produced between January and October, compared with 654, 743 Mt in the same period in 2017. The fairly high global copper prices which averaged US$ 6,598 and demand provided impetus for copper production. It is projected that annual copper output for 2018 will increase to over 800,000 Mt. Stable electricity supply also supported industrial production. In the last ten months of 2018 electricity generation increased by 12.6 % to 13.29 million Mwh from 11.86 million Mwh.

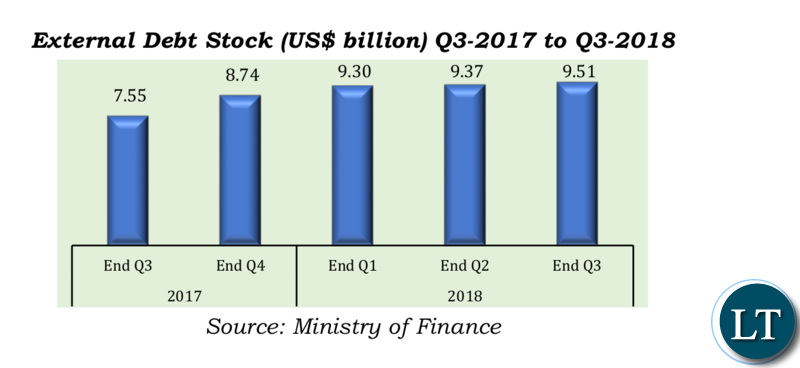

Public debt adjusts upwards in 2018 on account of new disbursements – Public debt (domestic and external debt) trended upward in 2018. External debt stock as at close of the third quarter was US$ 9.51 billion from US$ 8.7 billion at end December 2017. The upward adjustment in debt was on account of new disbursements on previously contracted financing, particularly for infrastructure. Total guaranteed debt at end September 2018 was at US$1.2 billion. External Debt service between January and September amounted to US$545.02 million. Final figures for 2018 will be issued in the annual economic report.

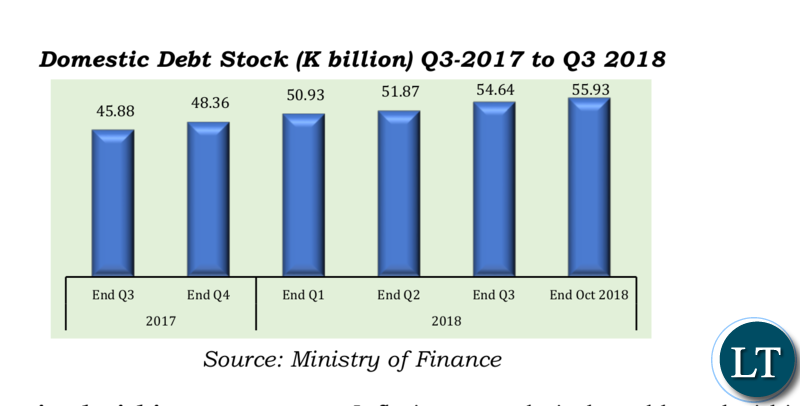

Domestic debt stock which composed of mainly government securities also rose to K54.6 billion as at end September 2018 from K48.36 billion at the end December 2017. Despite sustained efforts to dismantle domestic arrears, the figures trended upwards in 2018 mainly due to VAT refunds; and, capital spending – particularly in the road sector. As a result, domestic arrears were K14.7 billion at end of June from K12.7 billion as at close of 2017. In terms of domestic debt service, a total of K5.1 billion was paid out between January and September 2018. Final figures for 2018 will be issued in the annual economic report.

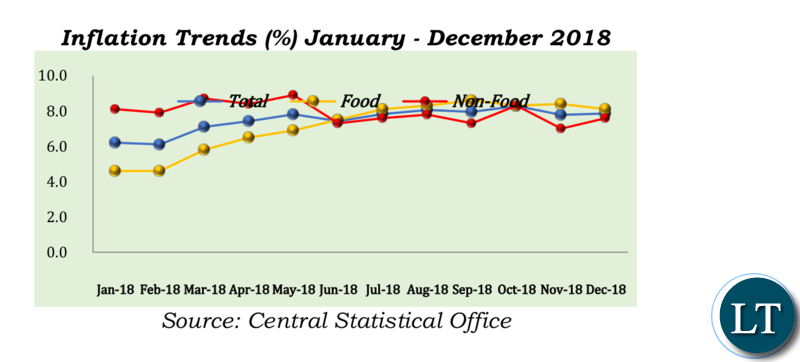

Inflation sustained within target range – Inflation was relatively stable and within the target range of 6-8 percent for most of part of the year. A slight headwind of Inflationary pressure during the early part of the third quarter triggered by depreciation of the Kwacha against tradable currencies and the passthrough effect of the domestic fuel price adjustment impacted on inflation. The highest inflation of 8.3 % was recorded in October and 7.9 % in December, 2018. Despite the edging up of inflation, 2018 average rate was sustained in the target range.

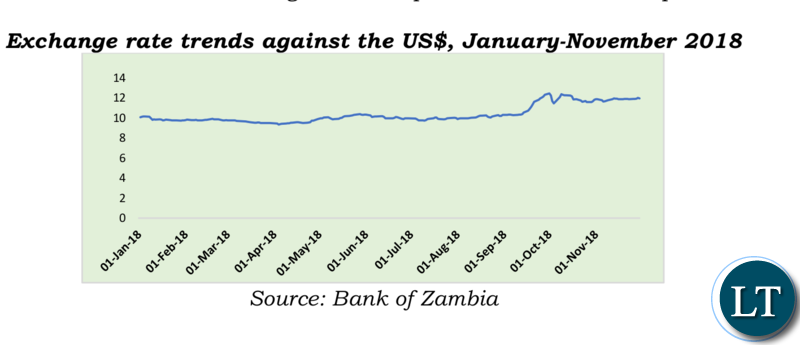

The Kwacha was relatively weak but stable in 2018 – The exchange rate of the Kwacha against major tradable currencies was stable most part of the year. Among other factors, the Kwacha weakened in the final third of the second quarter on account of higher than projected external debt service payments. A stronger US Dollar following the hike of the United States of America Federal Reserve Fund Rate, coupled with adverse market sentiment, were the major drivers for depreciation of the Kwacha and deterioration of the Purchasing Manager’s Index which, therefore, also impacted on overall business conditions. The Kwacha traded at an average of K10.33 per US$ during the period January to November from an average of K9.49 per US$ over the same period in 2017.

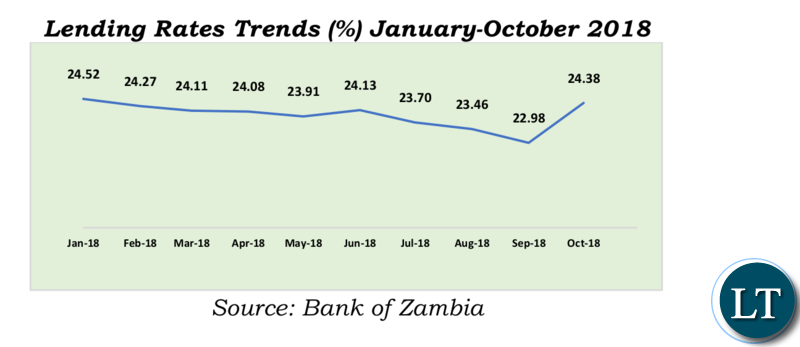

Lending rates edged downward marginally – Lending rates during the year showed a downward trend although still elevated in 2018 thereby constraining credit growth to the private sector. The continued liquidity constraints during the year, impacted on the slow downward movement in lending rates. As at November 2018, average lending rates marginally declined to 24.1% from 24.6% recorded as at end 2017. On the other hand, the Bank of Zambia adjusted the Monetary Policy Rate to 9.75% in November 2018 compared to 10.25% in November 2017.

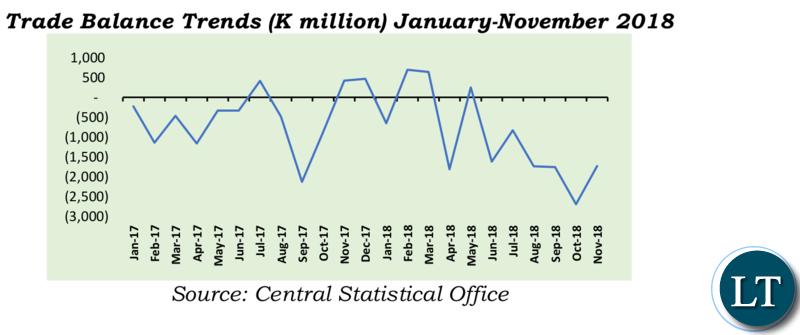

Trade deficit in 2018 – During the period January to November, 2018, Trade deficit widened to K11, 256 million compared to K6, 329 million recorded in same period in 2017. This weighed on the current account deficit which also widened. In nominal terms total exports of goods, however, during the period January to November increased by 24.5 % while imports of good increased by 28.8 %.

Notwithstanding higher than programmed debt service payments, gross national reserves remained around 2 months of import cover at US$ 1.73 as at August,2018.

REFORMS AND LEGISLATION IN 2018

During the year, we continued to implement austerity, economic stabilisation, and growth reforms. Several public service performance enhancement legislation was also enacted during the year under review. Key among the amended and enacted legislation was the Public Finance Management Act 2018, the Supplementary Appropriation Act of 2018, Credit Reporting Act 2018, National Health Insurance Act 2018, and the Public Private Partnership Act 2018.

Consistent with the target of improving domestic revenue mobilisation through enhanced provision of land titles, the National Land Titling Centre has beenestablished and is operational. The Zambia Credit Guarantee Scheme was also launched to facilitate affordable credit to SMEs.

Government also continued to roll out IFMIS [Integrated Financial Management Information System] and TSA [Treasury Single Account] of which 57 out of 62 MPSA’s [Ministries Provinces and Other Spending Agencies] have been put on the platform. This is critical for enhancement internal controls and facilitation of timely production of financial management reports for informed decision making.

In February, 2019, Zambia will be hosting the annual meeting of the East and Southern Africa Association of Accountants General [ESAAG]. As Government, we will take the opportunity to award certificates of recognition to Ministries, Provinces and Other Controlling Bodies that had no audit quarries in the current report of the Auditor General and those that have met non-tax revenue collection targets.

Most provisions in the Public Finance Management Act No. 1 of 2018 apply to both Central and Local Government Systems. To a great extent, the Public Finance Management Act No. 1 of 2018 will address the financial irregularities existent in local authorities. The wish of the Government is to see less and less public organisations both at central and local government level appearing in the Auditor General’s Report.

In addition, a code of corporate governance guidelines for the public sector is also being developed in order to effectively monitor performance of Boards of State Owned Enterprises and Statutory Corporations.

2018 BUDGET PERFORMANCE

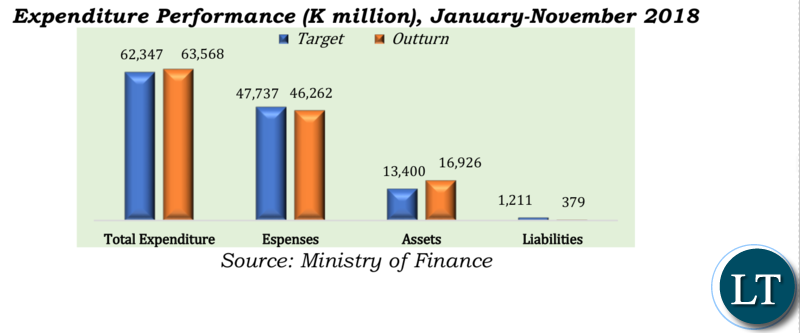

Budget execution in 2018 was broadly in line with annual target despite some fiscal challenges. Revenues and grants collections between January and November were above target by 4.2%. The performance was mainly driven by improved compliance in VAT and corporate tax especially from mining sector. Expenditure was also above target by 2% mainly due increase in interest payments on debt and spending on assets. Consequently, fiscal deficit outturn for the year is expected to be around 7%.

, January-November 2018")

ECONOMIC OUTLOOK FOR 2019

Positive and sustained macroeconomic stability and growth prospects for 2019 – In 2019 macroeconomic stability is projected to be sustained, aided by continued implementation of reforms and policies to support delivery of fiscal consolidation for sustainable and inclusive growth. Inflation is projected to remain with the medium-term range of 6-8 percent, robust growth of at least 4 percent is projected driven by both public and private sector investments, enhanced domestic revenues collection through continued implementation revenue boosting measures among other.

Downside risks to growth prospects include continued global trade tension, projected rise in crude oil prices due to continue geopolitical tensions, climate change related effects, and maintaining the fiscal deficit, weak credit growth and any failure to address domestic arrears may constrain growth and delayed implementation of reforms that will support growth.

Implementing reforms is challenging but the rewards are great. Unity of purpose makes it easier to achieve transformation and we in Government have led the way. Each key player must take the initiative to drive reforms at their level.

In order to sustain growth and create wealth, it is important that all stakeholders commit the legal reforms and the measures outlined in the economic stabilisation and growth programme.

Let me reiterate the commitment made by the President of the Republic of Zambia, Mr. Edgar Chagwa Lungu, to fellow citizens and to the international community that the austerity, fiscal consolidation, and economic stabilisation measures undertaken by the government are aimed at creating a strong foundation for improved economic management, sustained growth, and safeguarding the people’s welfare; through consistent and predictable public investments in education, health, social welfare and growth promoting programmes in accordance with the country’s aspirations outlined in the Seventh National Development Plan [7NDP].

As Government, we stand on firm grounds in our belief that Zambia’s prospects are bright. The country has sufficient talents to overcome the tide that is set against our economy, and together, we will achieve full stabilisation, strong growth, sustainable development goals and the Vision 2030.

Issued by:

Margaret D. Mwanakatwe, MP, MCC

Minister of Finance

Ridgeway, Lusaka

REPUBLIC OF ZAMBIA

{kind=link}

I am with you Margaret … Let’s roll

Why are we not surprised…you are a silly blind educated fooooool

RB’s ex girlfriend!!!!!

Magie PF brogers cant comprehend anything from your report. They are all about politics. Economical issues awe!! Hahaa patali. Trust me no one will give a good analysis all they will say is ROLL IT OUT.

I said that I don’t really believe this cooked up statistic and a few graphs plotted in excel. Where are 500 00 jobs and money in the pocket. That is what we should be talking about man!

Am not sure about this, was this statement meant for Zambians who put you in power or the IMF and foreign powers. Am not sure if our colleagues at Kulima tower would understand any of this. For Example, what does this statement mean?

in 2019, macroeconomic stability is projected to be sustained, aided by continued implementation of reforms and policies to support delivery of fiscal consolidation for sustainable and inclusive growth.

Does this mean anything, is this statement even refutable?? Give us systems and processes please that would get us there. I find the statement too academic. Hope Economists on this blog will unravel it for the majority us.

But lusaka stock exchange remains stagnant.

After ages of trashing Congolese for skin bleaching now they are at it. The finance looks like Meat Loaf’s twin brother. Would it be inappropriate at this stage to apologize to our Congo sisters and brothers?

Only people from Lusaka and copperbelt they will support your force statement,mind you we are tired of an empty promises.let Lusaka and copper belt dance for that useless promise.the opposite of that is to steal more in 2019.

A Drunkard giving forcasts really laughable

People with 3 to 4 brains are in Lusaka and copper belt so let them clap for you.us with 5 brains we are aware that it is the water under the bridge.

The economic outlook is usually bright but it is marred by corruption and bad governance along the way. Unless there is a significant improvement in the way we run our affairs as a country, we will not be able to generate sustainable wealth for our people. We must create an environment where positive figures must convert into tangible development for the masses. Hard working, honest Zambians must be rewarded with better standards of living instead of the endless “hand-to-mouth”struggles that they go through every day.

I have totally lost confidence in this government i even failed to read this obviously hollow statement, what a leadership God help us….

come 2021 you will dance to their campaign song and forget all you know abt hw they have messed and paa you will retain them into leadership

I don’t read such crap, from the visual impressions of graphical presentations. If even faked statistics are painting a gruesome picture, then know that the real picture is very very bad.

I think this minister is doing a good job and believe she has a very bright future in Zambia’s politics.

@ Rhapsody, You must be drunk to believe the lies from Magi!!

Keep believing the fake rosy stories. If you old enough you will understand that our politicians are great at showing us the rosy picture and never of the other picture which is reflected by the reality of things on the ground. This will not help the poor vendors and kaponyas who support them

I think what she meant was her personal outlook looks bright in 2019 not the country’s.

In a nutshell what the Minister of Finance is saying is God help us all in 2019. With increased debt repayments in 2019, new taxes the performance of the economy definitely needs a much more elaborate plan than what Maggie is proposing. What policies and interventions are going to stimulate investment and growth in 2019, not all these statistics that mean nothing. The impact of improved economic performance should be visible through better living standards and employment. If President Lungu wants to win 2021 he seriously needs to restructure his economic team starting with Minister of Finance, Economic Advisor, Boz Governor etc. The economy is bleeding and his team absolutely has no solutions…shame

Things are on the up. Good reason to go out and celebrate tonight!!! Mind the alcohol and don’t drive drunk…… HAPPY NEW YEAR. WELL DONE PF! PF FOR FOREVER ….!!!!

Mwanakatwe is a vested insider so lets wait and hear the more credible assessment and economic forecasts of independent bodies like Zambian economists,the IMF and Moody’s ratings.