By Samuel Chonya

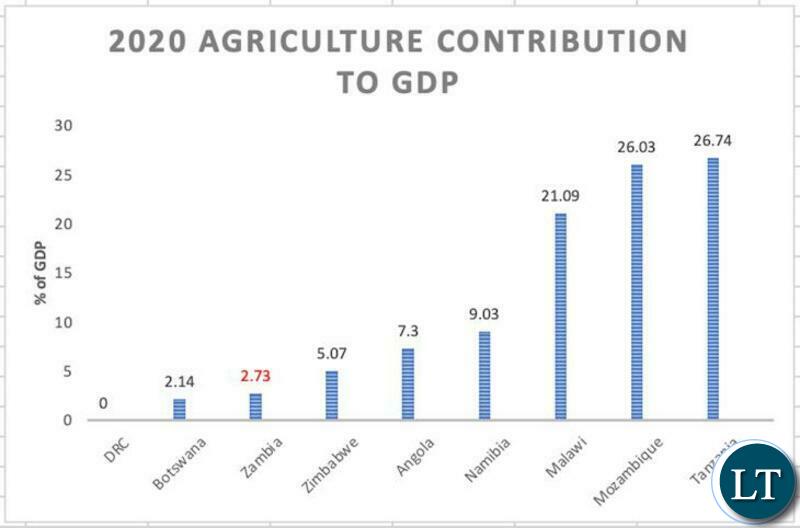

Agricultural development can lead to higher job and growth creation and stimulate economic development outside the agricultural sector. Zambia’s agricultural contribution to GDP in 2020 was disappointing 2.73% per cent, while neighbouring countries were Zimbabwe 5.07%, Angola 7.3%, Namibia 9.03%, Malawi 21.09%, Mozambique 26.03%, and Tanzania 26.74%. Zambia finds herself in the same category with Botswana at 2.14%, despite the Tsawanas having one permanent waterway, the Chobe River.

To paint how embarrassing the picture is, Zambia’s arable land from 2014 to 2018 was 3,800,000 hectares of fertile soils out of the entire country’s land area of 74,339,000 hectares. The country has 3 vast natural lakes, in northern Zambia, there are Bangweulu, Mweru, and Lake Tanganyika [one of the deepest natural lakes in the world]. Zambia also has 3 major rivers, the Zambezi [Africa’s fourth-largest river system], the Luangwa, and the Kafue River, with over 27 formidable tributaries within her borders.

The DRC can be excused because there is war within her borders. The Tswanas too can be excused, considering the Kalahari Desert occupies almost all Botswana, leaving them with an arable land of 259,600 hectares, and making do with only one River, The Chobe. So why then is Zambia’s agriculture sector failing to contribute more to the nation’s GDP and compete to surpass Malawi and Tanzania? Why does Zambia, despite her millions of hectares of arable land, compete with war-torn DRC and arable land strapped Botswana?

Zambia’s agriculture finance failures

There has been an observation by not only those heading cooperatives in the agriculture sector but also scholars, stating insufficient agricultural finance as a major impediment in agriculture development. As a result, since the early 1960s, the financing of the agriculture sector has seen the rise and fall of Zambia’s government-initiative credit programmes carried out by actors in the agriculture sector. These efforts have seen the creation of credit programs, including the Agriculture Finance Company, Agriculture Credit Management Program, Credit Organisation of Zambia, Marketing Credit Revolving Fund, and the Zambia Agriculture Development Fund among many others. Despite some initial varying levels of success, eventual failure was inevitable to all these credit programs.

The main sources of agriculture financing in Zambia are contract farming, private companies, friends/relatives/informal money lending, and farmers’ unions/cooperatives. Lending from commercial loan sources to Zambia’s agriculture sector has contributed the highest share of non-performing loans at 26%. Predominantly, non-performing loans from the agriculture sector arise because Zambia’s farmers have inadequate risk management mechanisms and are most exposed to production risks, institutional risks, financial risks, and market/price risks. Any one of these risks befalling farmers affects their margins, tips them into losses and puts them in a space they cannot meet their obligations. Therefore, banks often request collateral to mitigate adverse selection and moral hazards.

Adverse selection in Zambia is high, as many farmers lack sufficient collateral to securitise against loans. More so, lenders cannot differentiate between borrowers with varying credit risks before providing loans.

Financial institutions also face moral hazard in Zambia, where many borrowers engage in activities that may lead to loans not being repaid or use loans for purposes not agreed with financial institutions.

Commercial loans to the sector remain inadequate due to the factors mentioned above, not because banks do not have the funds, but because they are unwilling to take risks that can befall a farmer. Therefore, in the effort to participate in the agriculture sector, and minimise non-performing loans, commercial banks are likely to partner with other firms, including those leasing equipment to own, or out-growers. However, these sources are limited, and most farmers still have perennial challenges in accessing finance.

The challenges

Little has been undertaken to understand the characteristics that lead to the failure of Zambia’s agriculture efforts of making finance continuously accessible.

However, in Zambia, start-up capital is a persistent challenge, as the country has never been on top of policies responsible for creating conducive environments that allow the agriculture sector to thrive.

There are several reasons policy makers are getting this wrong, and many of these are specific to a given country, district, or institution. There are three policy-making zones that have an impact on agricultural and rural finance: agricultural sector policy, financial sector policy and macroeconomic policy. The fact that these are different policy groups engender a danger that the special needs of farmer categories could be overlooked, or as is more likely, policies developed can be partially in conflict. This can be said to be Zambia’s position and explains why the country’s agriculture contribution to GDP stands at 2.73%. Studies show that all Zambia’s neighbours except for war-torn DRC, have to an extent crafted for themselves a mutually supportive agricultural environment of policy according to their environmental circumstances.

Recommendations

Zambia needs to take an innovative approach in the agricultural sector to find solutions to challenges unique to the country on a sectoral level. Policymakers responsible for agriculture, financial and macroeconomic policies need to establish interactions with the leading sub-sector intermediaries. This interaction helps establish and enhance knowledge bases in the agricultural sector regarding marketing, financing, risk management and technical expertise, all of which are critical elements in enabling agricultural finance.

This article is a synopsis of the research thesis I undertook, to understand the complexities of Zambia’s agriculture sector and how agriculture finance remains a challenge, including recommendations to overcome such challenges.

The Author is an international development economist with over ten years of experience in development practice in the UK. He has a consulting portfolio comprising the British Government with DEFRA, DCMS and APHA, the NHS and charitable organisations. He has a PhD in International Development and holds an MSc from the University of South Wales, and a Fellow of the ACCA. He can be contacted on [email protected] mobile: +44758 467 1735/+26096 104 1555

{kind=link}

The non-existent agricultural policies of the PF government, who were more interested in filling their pockets than governing the country, and the greedy banks making loans too expensive with 25% interest rates – that’s why farming isn’t fun in Zambia!

If successive Zambian governments from UNIP to PF had been smart they would have invested heavily in agriculture and Zambian would have been the breadbasket of the world, minting daily dollars from exports and contributing massively to the economy, not the paltry 2.73%. Zambia is blessed with abundant water, nice climate, plenty land, peace and stability, lots of starving neighbors who would pay dollar to get hold of our food. But no, our leaders have perfected the art of begging from overseas and working to develop and benefit from our God given resources is seen as unnecessary hard work. I am confident the new government of UPND will take a critical look at agriculture and see it for what it is; a veritable source of unlimited money and game changer. Forget about copper and other metals…

Our commercial farms just like the mines are secretly feeding the Europeans and the scraps are reserved for the local market. We see Zambian produce in some of the top supermarket chains such as Waitrose, Tesco and Sainsburys sold as type 1 fruit and veg, meaning it’s top quality. One wonders if Zambians are capable of identifying what type 1 fruit and veg looks like.

fantastic article

Very provocative thesis which deserves attention from the incoming government to unlock Zambia’s potential in agriculture. Financing and access to overseas markets notwithstanding a key area for analysis is value added agricultural exports. Export of raw fruits and vegetables has limited profit and requires a very cost prohibitive refrigeration chain to get product to market. Small holders must identify value added opportunities

It is really a no brainer and agriculture is answer to our economic recovery. Mwanawasa as farmer tried. I hope HH can transform sector since is a farmer.

We have ready market near by in Angola and DRC but even a bigger one in China so what is our problem? Leadership and focus. Hope we now have right leader.

Great article Chonya

I wouldn’t knock international trade .It is vital to any economy.